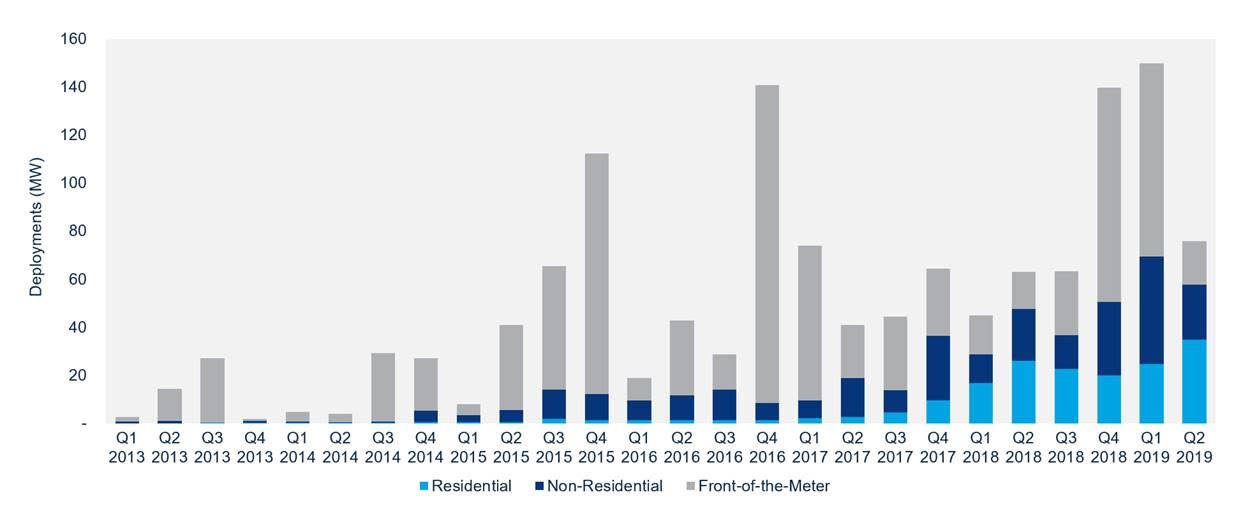

The second quarter of 2019 was the largest quarter on record for residential energy storage, according to the new U.S. Energy Storage Monitor from Wood Mackenzie Power & Renewables and the U.S. Energy Storage Association (ESA). The United States installed 35 MW of residential storage in Q2 2019.

Also of note, the U.S. market installed a total of 75.9 MW of front-of-the-meter (FTM) and behind-the-meter (BTM) storage in Q2 2019, a 20% increase from Q2 2018.

The residential storage market was up 41% quarter-over-quarter in megawatt terms, a result of rising customer interest and support incentives in more state markets. The previous megawatt record for residential storage additions was set in Q2 2018 with 26 MW deployed. The FTM storage market had a relatively quiet Q2, with 18 MW deployed after two consecutive quarters when the FTM market topped 80 MW. The FTM pipeline, however, grew by 66% in Q2, driven by continued large-scale utility procurements and developer interest in ISO markets shown by surging interconnection requests.

“The long-term growth trends of energy storage deployment nationwide are encouraging and consequential for stakeholders, and for all electricity users who want and deserve a more resilient, efficient, sustainable and affordable electricity grid,” said Kelly Speakes-Backman, CEO of ESA. “Federal lawmakers should take note that they can help to build upon this growth, and indeed result in a 16% upside for the U.S. storage market, by providing a long term policy direction for every region of the country by making energy storage an explicit, standalone criteria in the federal ITC.” As written, federal ITC qualifications include energy storage solely when coupled with solar power.

FIGURE: U.S. Quarterly Energy Storage Deployments by Segment (MW) / Source: Wood Mackenzie Power & Renewables

“The nascent energy storage market in the U.S. continues to grow in fits and starts,” said Dan Finn-Foley, head of energy storage for Wood Mackenzie Power & Renewables, “but signposts such as the record residential storage quarter, massive FTM pipeline growth, and innovative policies such as the Massachusetts clean peak standard point towards an industry that is maturing and should stabilize at scale over the next two years.”

Q2 2019 saw 165 MWh of storage brought online, with BTM storage (including non-residential) contributing 83% of the megawatt-hours. California led the residential and non-residential markets in megawatt-hour terms, with Hawaii in second place on the residential side and Massachusetts coming in second for non-residential BTM storage. Texas and Maine were the quarter’s top states for FTM storage at 10 MWh each.

FTM project delays and a weaker-than-expected H1 in some BTM markets caused the U.S. energy storage outlook for 2019 to fall to 478 MW, which represents an increase of 54% over the 311 MW deployed in 2018.

The storage market will grow by roughly tenfold between 2019 and 2024, bolstered by supportive policy structures and new opportunities for storage to provide wholesale market services.

Key findings from the report:

- 75.9 MW of energy storage was deployed in the United States in Q2 2019, falling 49% QOQ

- 165 MWh of storage was brought online in the United States in Q2 2019, falling 40% QOQ

- In Q2 2019 FTM storage deployments dropped 77% QOQ in MW terms and rose by 17% YOY

- In Q2 2019 BTM storage deployments dropped 17% QOQ in MW terms and rose by 21% YOY

- BTM (residential and non-residential) storage accounted for 83% MWh deployed in Q2 2019

The most recent version of the Energy Storage Monitor is available here.

News item from WoodMac

Tell Us What You Think!